Market Insights

Market Insights: 30. April 2025

Smart Home of the Future

Consumers are setting the direction

After two years of stagnation, 2024 brought a turnaround: the Home & Consumer Tech market regained momentum worldwide. In 13 key European markets, smart home products grew by 8 percentage points**. Despite a weak economy and political uncertainty. A clear sign that consumer interest in smart technology remains strong and that this category continues to offer significant potential for premiumization. Major domestic appliances (MDAs) in particular posted strong growth of 21 percent**, making them a key driver of overall growth. Smaller appliances, health products, and home control systems also contributed to the upswing, each growing by 8 percent**.

Regional differences as a purchasing criterion

Acceptance of smart products varies significantly from region to region. Reasons for this include product affordability, the quality of internet connections, and data privacy concerns. A comparison shows that although Germany and Turkey have similar attitudes toward data privacy, their market shares for smart products are far apart. Germany benefits from good, stable internet speeds and moderate monthly internet costs. Here, the value share of smart products is 38 percent. In Turkey, on the other hand, where fixed internet speeds are lower and monthly costs are cheaper, the value share reaches only 23 percent.

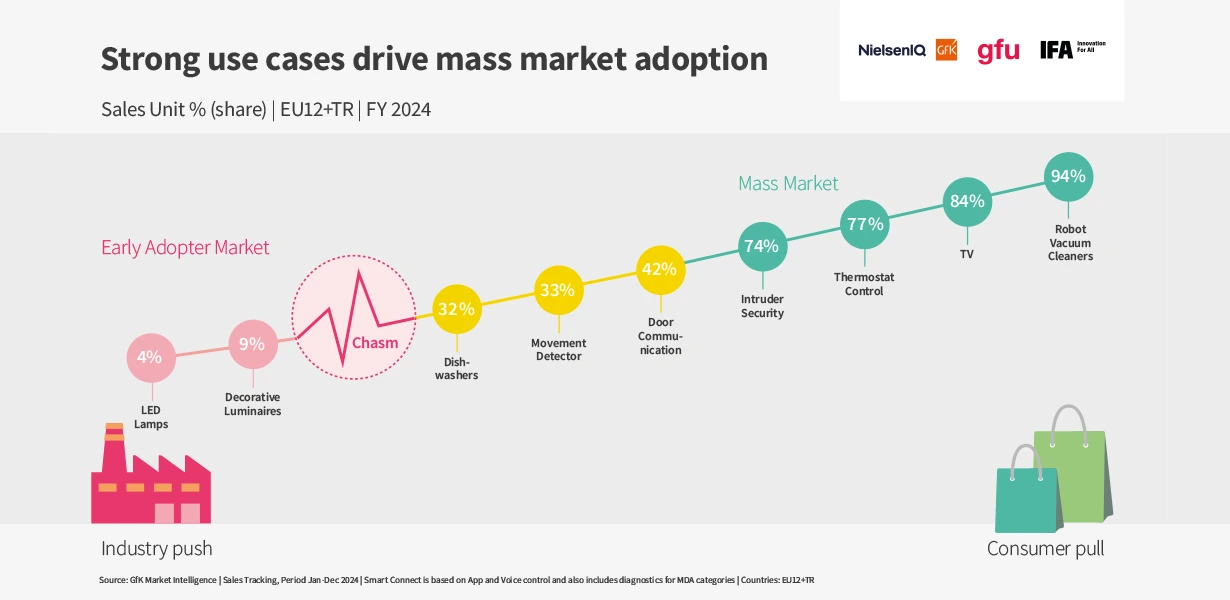

What drives consumers

Innovation-minded consumers are willing to pay a premium for smart products that offer convenience and ease of use. 57 percent[1] cite increased convenience as one of the main reasons for their purchase decision. Products that make everyday life easier are particularly in demand – especially when it comes to cleaning and cooking. Smart robot vacuum cleaners and dishwashers, with market shares of 94 percent[2] and 32 percent[2] respectively, are among the most popular appliances. The latter category in particular has gained significantly in importance over the past three to four years.

In addition to convenience, users are increasingly paying attention to energy efficiency (46 percent)[1] and long-term cost savings (36 percent). This trend is reflected, among other things, in the strong growth of energy-efficient major domestic appliances: the share of appliances certified as “Energy Class A” rose from 12 percent in 2022 to 29 percent by the end of 2024. Smart thermostats are also enjoying growing popularity and have achieved a high acceptance rate of 77 percent[2].

Beyond the aspect of energy savings, consumers value integration into existing smart home solutions as well as comprehensive security features. Significant growth between 2019 and 2024 is particularly evident in the area of smart security products – such as burglar alarms, motion detectors, and door communication systems. Nevertheless, the potential remains substantial: according to the NIQ-GfK “Consumer Life” study, 54 percent of respondents say that a smart security product would be their first purchase in this category.

AI as an enabler

The integration of artificial intelligence marks the next stage of evolution for smart products. While AI is not always the decisive purchase criterion, it significantly improves the functions consumers value most: better performance, optimized energy savings, and personalized routines. From robot vacuum cleaners to washing machines, AI-powered products deliver superior navigation and an improved user experience.

Challenges and opportunities

Despite positive trends, obstacles still stand in the way of the broad adoption of smart products. High costs (45 percent)[1] and data privacy concerns (41 percent)[1] remain key barriers. To increase market acceptance, greater brand diversity, a broader product offering, and above all more affordable prices are needed. Compelling applications that offer concrete benefits are crucial. A good example is smart TVs, which are particularly successful with a market share of 84 percent[2]: AI-based upscaling, integrated streaming services, and intelligent features align precisely with users’ wishes. Manufacturers can use these insights to address growing demand in a targeted way – and develop products that combine convenience, security, and cost efficiency.

Sources:

[1] NielsenIQ Smart Home Monitor Study Netherlands

[2] NielsenIQ Market intelligence Sales Tracking Period Jan-Dec 24 vs PY, Countries: EU12+TR

About the collaboration

Based on a partnership between NIQ/GfK, gfu, and IFA Management, we provide you with regular updates on market developments and trends in the Home & Consumer Tech sectors. Interesting insights, current market figures, consumer trends, and much more are professionally prepared for you from the sources of the three expert partners.